Why Passkeys Are Quietly Replacing Your Passwords

If you have logged into an account recently and been offered the chance to sign in with your face, your fingerprint, or a tap instead of typing a password, you ...

Building a Morning Routine That Actually Sticks

Search for advice on morning routines and you will drown in the same intimidating template: wake at five, meditate, journal, exercise, cold shower, read, plan t...

Darina Laurent·Jul 20, 2026

Darina Laurent·Jul 20, 20262

Active Authors

27

Articles Published

5

Topics Covered

120K+

Monthly Readers

Latest Posts

Fresh stories from our community writers

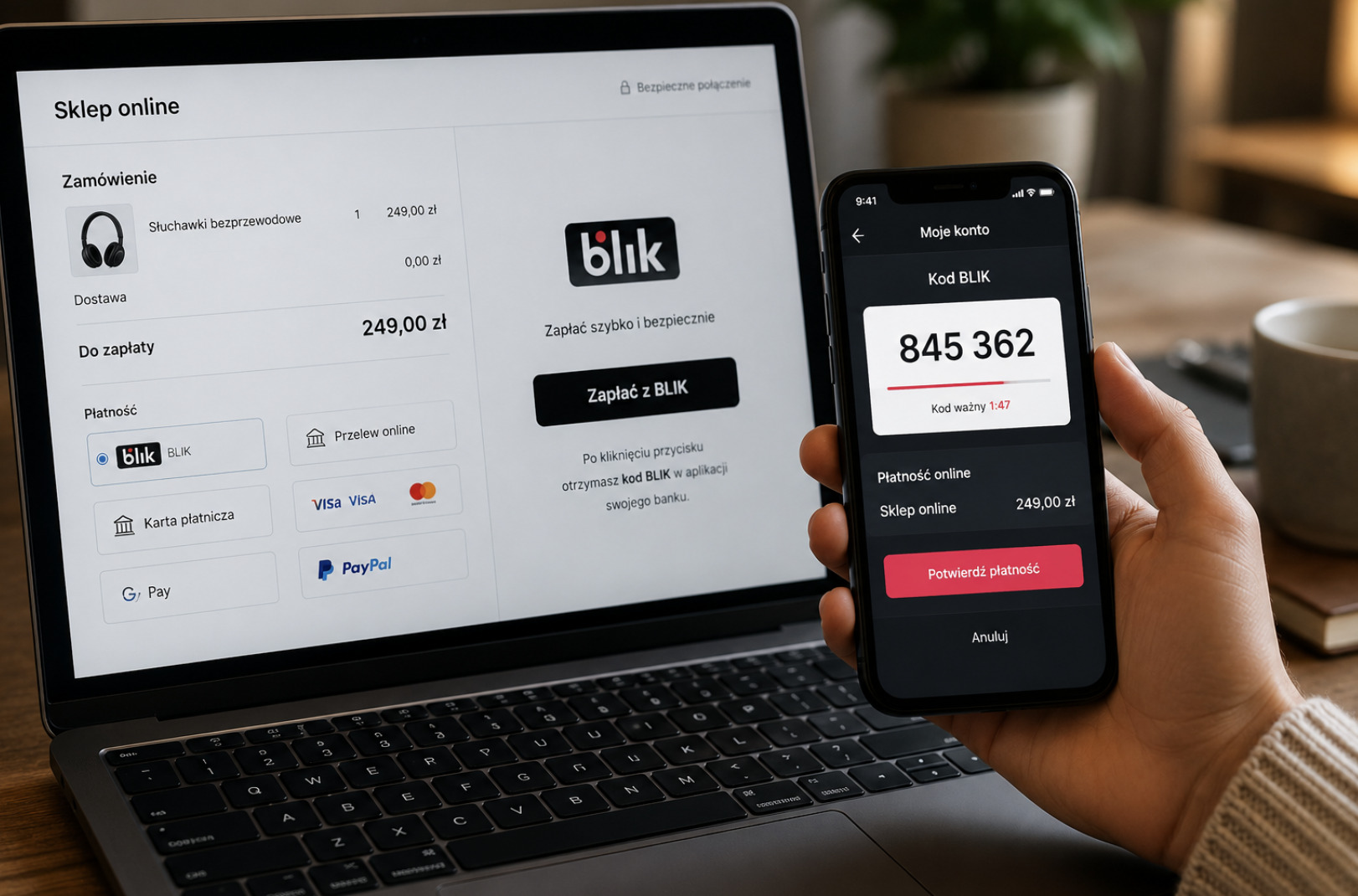

How BLIK Works for Online Payments in Poland

BLIK is the payment system that quietly transformed how Poland pays online. What began as an initiative by Polish banks working together has become a national h...

Darina Laurent

Why AI Agents Are Quietly Becoming the Next Big Tech Shift

For the last few years, the face of artificial intelligence has been the chatbot: you ask, it answers. It writes your email, summarises your document, explains ...

Better Sleep Is the Quiet Upgrade Most People Keep Ignoring

We treat sleep as the thing we cut when life gets busy — the negotiable hours, the buffer we raid to make room for work, screens, or one more episode. It is a s...

Darina Laurent

The Machinery That Turns Small Bets Into Life-Changing Jackpots

Every so often, an online slot pays out a sum large enough to change someone's life — a figure with many zeros, won from a stake of a few coins. These are progr...

Darina Laurent

How to Deposit and Withdraw Crypto at Online Casinos

Moving money in and out is the part of online gaming that trips people up most, and crypto adds its own quirks — networks, confirmations, and the occasional irr...

How to Build a Real-Time Crypto Price Tracker with AJAX

A real-time crypto price tracker is one of the best projects for learning modern web data flows. It touches everything: external APIs, polling versus streaming,...

Darina LaurentShare your expertise with

thousands of readers

Write about anything — tech, lifestyle, culture, travel, science. Postpear is for every voice, every perspective.

Fashion & Style

Why Everyone Suddenly Wants Tailoring Again — and What That Says About a Culture Tired of Comfort

If you have walked past a shop window in any major city in the past six months, you have probably noticed a small but very specific change. The mannequins are w...

Darina Laurent

Why Quiet Luxury Became the Dominant Fashion Mood Online

For years internet fashion culture was dominated by visibility. Logos grew larger, streetwear collaborations became louder and social media rewarded outfits des...

Darina LaurentGames and Online Entertainment

How BLIK Works for Online Payments in Poland

BLIK is the payment system that quietly transformed how Poland pays online. What began as an initiative by Polish banks working together has become a national h...

Darina LaurentThe Machinery That Turns Small Bets Into Life-Changing Jackpots

Every so often, an online slot pays out a sum large enough to change someone's life — a figure with many zeros, won from a stake of a few coins. These are progr...

Darina LaurentHow to Deposit and Withdraw Crypto at Online Casinos

Moving money in and out is the part of online gaming that trips people up most, and crypto adds its own quirks — networks, confirmations, and the occasional irr...

What Are Megaways Slots, and Why Do British Players Love Them?

The way Britain spends its downtime has moved online. Streaming, mobile gaming, podcasts and social apps all compete for the same pockets of free time on the so...

Tech & Innovation

Why Passkeys Are Quietly Replacing Your Passwords

If you have logged into an account recently and been offered the chance to sign in with your face, your fingerprint, or a tap instead of typing a password, you ...

Why AI Agents Are Quietly Becoming the Next Big Tech Shift

For the last few years, the face of artificial intelligence has been the chatbot: you ask, it answers. It writes your email, summarises your document, explains ...

How to Build a Real-Time Crypto Price Tracker with AJAX

A real-time crypto price tracker is one of the best projects for learning modern web data flows. It touches everything: external APIs, polling versus streaming,...

Darina Laurent

The End of the Search Box — What We Will Lose When Asking Becomes Conversation

There is a question you can ask yourself that will date the moment more precisely than almost any other piece of self-observation. When was the last time you ty...

Movies

Why Audiences Are Getting Tired of Perfect Streaming Shows

For more than a decade, streaming platforms have operated under the assumption that audiences primarily want efficiency. Faster pacing, cleaner storytelling, co...

Darina Laurent

“Gone with the Wind” — Why It Remains a Cultural Icon

Gone with the Wind is one of those rare works that transcends its time to become something bigger than just a novel or a film. It’s a cultural myth—an enduring ...

Darina LaurentLifestyle & Wellness

Why Walking Is the Most Underrated Form of Exercise

In a wellness culture obsessed with intensity — the harder workout, the fancier equipment, the more punishing regimen — the most effective thing many people cou...

Darina LaurentBuilding a Morning Routine That Actually Sticks

Search for advice on morning routines and you will drown in the same intimidating template: wake at five, meditate, journal, exercise, cold shower, read, plan t...

Darina LaurentBetter Sleep Is the Quiet Upgrade Most People Keep Ignoring

We treat sleep as the thing we cut when life gets busy — the negotiable hours, the buffer we raid to make room for work, screens, or one more episode. It is a s...

Darina Laurent

The Slow Disappearance of Boredom — and What We Quietly Lost When We Stopped Letting Ourselves Be Bored

There is a small experiment you can run on yourself, and the result of it will tell you more about the present moment than almost any other piece of self-observ...

Community Authors

Real people, real voices — not just an editorial team

Share Your Story

Got something to say? Postpear gives every writer a platform to be heard.

Start writing →Build Your Audience

Connect with readers who care about your topics. Grow your following on Postpear.

Meet our authors →Quality Content

We maintain high editorial standards. Read our guidelines to ensure your work shines.

View guidelines →