How BLIK Works for Online Payments in Poland

BLIK is the payment system that quietly transformed how Poland pays online. What began as an initiative by Polish banks working together has become a national h...

Community Author · July 17, 2026

BLIK is the payment system that quietly transformed how Poland pays online. What began as an initiative by Polish banks working together has become a national habit so ingrained that, for a great many Poles, it is simply the default way to pay on the internet. If you shop, bank, split a bill or fund an account online in Poland, you have almost certainly used it, and if you are new to the country's digital life, it is one of the first things worth understanding. Its rise is a genuine case study in how a well-designed local solution can outpace international alternatives in its home market, and its mechanics are refreshingly simple once you see them.

What BLIK is

BLIK is a Polish mobile payment system that lets people pay online and in shops, and send money to one another, directly through their banking app. Rather than typing card numbers into a website, a user generates a short, temporary code in their bank's app and uses it to authorise the payment. It was created by Polish banks collaborating on a shared standard, and that origin is a large part of its strength: because BLIK is built into the banking apps most Poles already use every day, adopting it required no new account, no separate wallet and no unfamiliar third party to trust. That deep integration with the existing banking system is exactly why it spread so quickly and so widely across the country.

The result is a payment method that feels less like a separate tool and more like a native feature of Polish banking itself. For users, it turned online payment from a matter of hunting for a card and copying numbers into something that takes a few seconds inside an app they already have open.

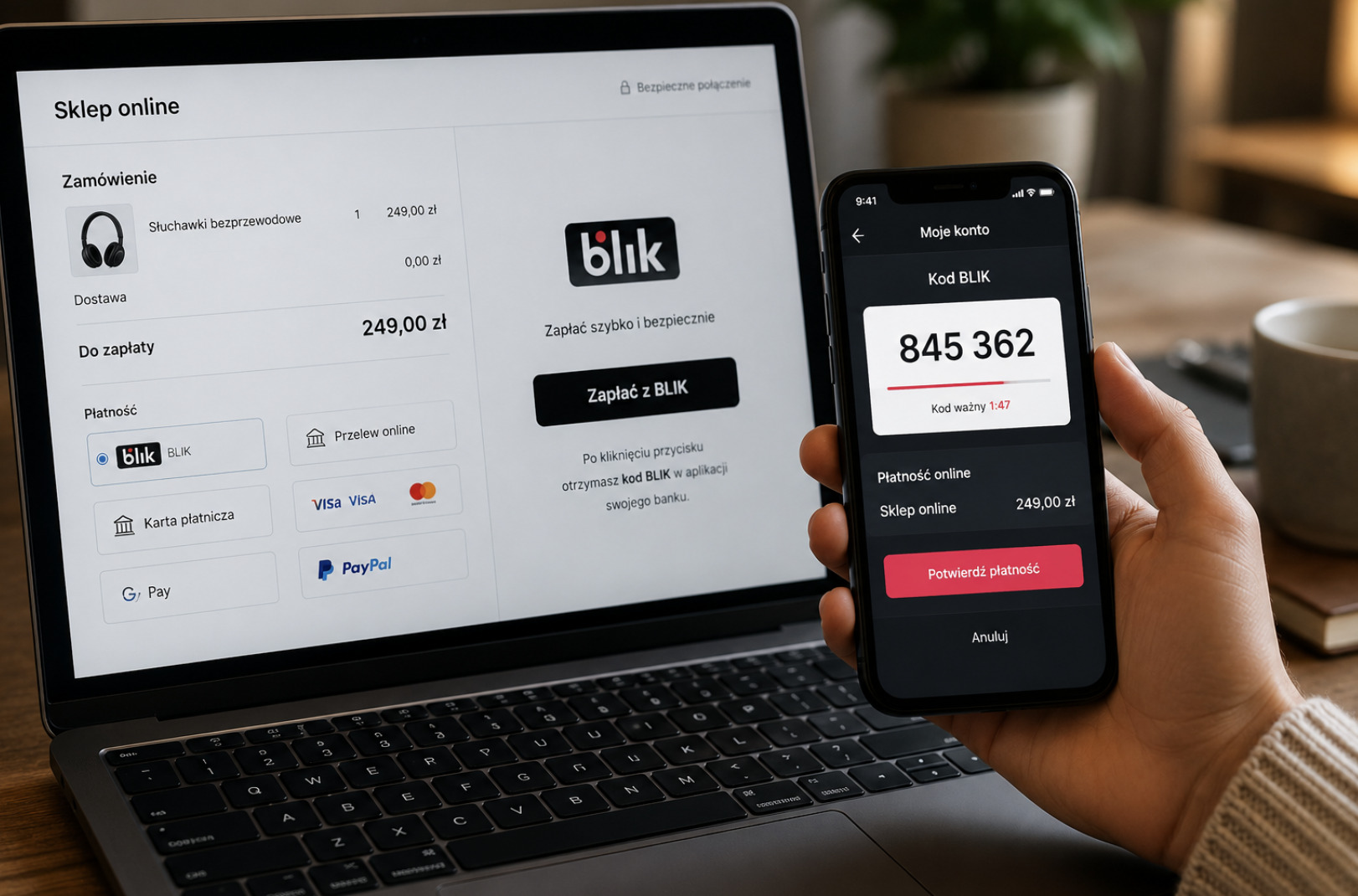

How a BLIK payment works, step by step

The mechanics are simple, and their simplicity is central to the appeal:

At an online checkout that supports BLIK, you choose it as the payment method.

You open your banking app, where a six-digit BLIK code is generated, valid for only a short time.

You enter that code on the payment page.

You confirm the transaction in your banking app, typically with a PIN or a biometric approval such as a fingerprint or face scan.

The payment is then taken directly from your bank account, and the whole process takes only seconds. Because the code is temporary and the final confirmation happens inside your own banking app, your card and account details are never exposed to the merchant you are paying. This flow — generate a code, enter it, confirm in the app — is identical whether you are paying a shop, a subscription or another kind of online service, which is why Polish users find it so quick and familiar across the entire web. Services aimed at Polish players, from retailers to entertainment platforms such as Crazy Tower Casino, commonly list BLIK among their supported methods precisely because so many Poles simply expect to be able to pay this way.

Why BLIK became so dominant in Poland

Several factors combined to drive BLIK's remarkable adoption, and understanding them explains why it succeeded where imported alternatives struggled. It is convenient, needing only the banking app already on the phone and a short code rather than card details. It is fast, with payments settling in seconds. It is trusted, because it comes from the Polish banks themselves rather than an unfamiliar foreign intermediary, and it keeps financial details private by handling confirmation inside the banking app. It also unified what had been a fragmented experience: instead of juggling many different payment tools, Poles gained one simple method accepted across their banks and a huge range of merchants.

That combination of convenience, speed, trust and near-universal acceptance is why BLIK moved from novelty to national standard in a relatively short time. It is a reminder that the best payment method in a given market is often not the biggest global brand but the one that fits local habits and infrastructure most naturally — and BLIK, built by and for the Polish banking system, fits Poland exactly.

Strengths and things to know

BLIK's strengths are its speed, simplicity, privacy and acceptance among Polish banks and merchants. There are a few practical points worth keeping in mind alongside those strengths. It is a domestic system built around Polish bank accounts, so it is a local method rather than an international one — its acceptance is centred on Poland. Each code is short-lived by design, which is a deliberate security feature, so a payment must be completed promptly before the code expires and a new one has to be generated. And, as with any payment method, sensible security habits matter: only confirm transactions for purchases you actually recognise, and be alert to scams that try to trick users into approving a BLIK payment or handing over a code.

None of these points diminishes BLIK's usefulness; they simply describe how to use it well. For everyday payments within Poland, its speed and simplicity are hard to beat, and its limitations rarely come into play for ordinary transactions.

Using BLIK safely

BLIK is secure by design — temporary codes, in-app confirmation and no exposure of card details all work to protect the user. The most important safeguard, though, is behavioural, because no payment method is immune to social engineering. Never share your BLIK code with anyone, and only approve a payment in your banking app when you were the one who initiated it. A well-known scam involves someone posing as a friend, a buyer or an official and asking a victim to approve a BLIK transaction or reveal a code; a genuine payment is always one that you started yourself. Treating the six-digit code like a one-time key that only you should ever see or use keeps BLIK as safe in practice as it is by design. If a request to approve a payment ever arrives unexpectedly, the safe response is to stop and verify independently rather than to approve it under pressure.

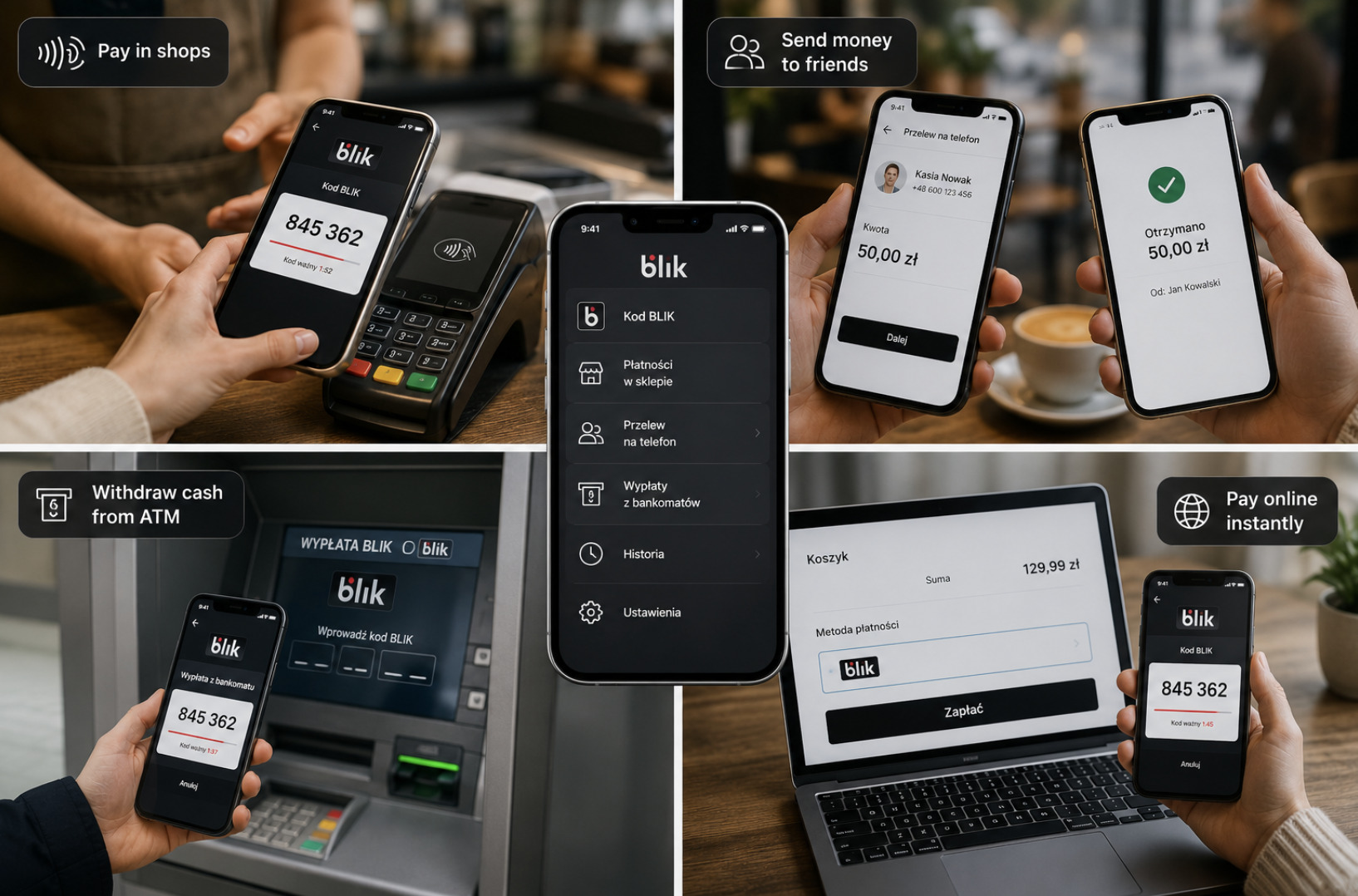

BLIK beyond online checkouts

Although paying at online checkouts is the use most people associate with BLIK, the system does considerably more, which helps explain how deeply it is woven into Polish daily life. The same six-digit code can be used to pay in physical shops at the till, turning the phone into a payment card without any card being present. It also powers person-to-person transfers: you can send money to another person using only their phone number, quickly and without needing their bank details, which has made splitting bills and repaying friends effortless. In many places it can even be used to withdraw cash from an ATM by generating a code rather than inserting a card.

This breadth matters because it means BLIK is not a niche online tool but a general-purpose payment habit. A Pole who uses it to withdraw cash, pay at a shop and send money to a friend already trusts and understands the same mechanism they then use to pay online. That familiarity lowers the barrier to using it for any new online service, because there is nothing new to learn — it is the same code, the same app, the same quick confirmation they use for everything else.

Why BLIK suits online services so well

There is a specific reason BLIK became such a natural fit for funding online accounts, beyond its general convenience. When paying an online service, users often prefer not to hand over card numbers or bank credentials, both for privacy and to limit their exposure if anything ever went wrong. BLIK solves this cleanly: the payment is authorised inside the user's own banking app, and the service receives the funds without ever seeing any financial details. That separation is exactly what a cautious online payer wants, and it is delivered without any extra effort on the user's part.

Combined with the fact that nearly every Polish adult already has BLIK built into their banking app, this makes it an obvious choice for online services to support and for users to reach for. For the person paying, it means funding an account or completing a purchase directly from a trusted bank, quickly and privately, without adopting any new tool. Few payment methods match that blend of trust, speed and privacy as neatly in the Polish market, which is precisely why it has become the expected option across so much of the Polish web.

How BLIK compares with cards and e-wallets

It helps to see where BLIK sits alongside the other ways Poles pay online. Compared with entering a debit or credit card, BLIK keeps card details entirely out of the transaction and confirms inside the banking app, which is both faster and more private than typing a long card number and a security code. Compared with an e-wallet, BLIK requires no separate account to create and fund — it works straight from the banking app the user already has — so there is nothing extra to set up. Compared with a traditional bank transfer, it is far quicker and simpler, generating a code and confirming in seconds rather than copying account numbers.

The picture that emerges is of a method whose strengths are convenience, speed, privacy and near-universal local acceptance, with its main limitation being that it is domestic rather than international. For everyday payments within Poland, that trade-off is easily worth it, which is why BLIK, rather than any global alternative, became the default. It is a clear example of a local solution winning its home market by fitting local habits and infrastructure better than anything imported could.

The takeaway for players in Poland

Pulling the threads together, BLIK earns its place as the default Polish payment method for a clear and consistent set of reasons. It is built into the banking apps almost everyone already uses, so there is nothing new to adopt. It confirms payments inside that app, keeping card and account details private. It is fast, settling in seconds, and it is accepted almost everywhere online in Poland, as well as in shops, at ATMs and for transfers between people. Its main limitation — that it is domestic rather than international — rarely matters for everyday Polish payments.

For a player in Poland weighing how to fund an online account or complete a purchase, that combination makes BLIK a sensible baseline: quick, private, trusted and already at hand. Used with reputable, regulated services and a little everyday caution about scams — never sharing a code, only approving payments you started — it remains one of the most convenient and dependable ways to pay online in the country. Its success is a reminder that the payment method that wins a market is usually the one that fits how people there already live and bank, which is exactly what BLIK was built to do.

Frequently asked questions

Is BLIK instant? Yes. BLIK payments are processed in seconds, taken directly from your bank account once you confirm in your banking app. Speed is one of the main reasons it became so widely used across Poland.

Does BLIK share my card details with the merchant? No. You authorise the payment with a temporary code and confirm inside your own banking app, so your card and account details are never exposed to the merchant you are paying.

Can I use BLIK outside Poland? BLIK is a Polish system built around Polish bank accounts, so it is primarily a domestic method. Its acceptance is centred on Poland rather than being a broad international option.

What happens if my BLIK code expires? Each code is valid only for a short time as a security measure. If it expires before you complete the payment, you simply generate a new one in your banking app and enter that instead.

Is BLIK safe to use? Yes, it is secure by design, using temporary codes and in-app confirmation without exposing card details. The main risk is social-engineering scams, so never share your code and only approve payments you started yourself.